2022 Tax Guide for Prosper Investors

It’s tax season, and to help Prosper retail investors navigate the process, we’ve created the 2022 Prosper Tax Guide.

It’s tax season, and to help Prosper retail investors navigate the process, we’ve created the 2022 Prosper Tax Guide.

Peer-to-peer lending pioneer expands suite of home equity products amid strong performance, supporting more customers across the credit spectrum SAN FRANCISCO – October 24, 2022

Today we are sharing performance data from the Prosper Portfolio for August 2022. Highlights from the Prosper Performance Update – August 2022: Portfolio insights and

NO PURCHASE NECESSARY TO ENTER OR WIN. A PURCHASE WILL NOT IMPROVE YOUR CHANCES OF WINNING. DISPUTE RESOLUTION NOTICE: BY ENTERING, TO THE FULLEST EXTENT PERMITTED

We know how important your credit score is to your financial well-being. That is why we have brought your FICO® Score to your Prosper account,

It’s tax season, and to help Prosper retail investors navigate the process, we’ve created the 2021 Prosper Tax Guide. This guide has general information about the 1099 tax form(s) you may receive from Prosper.

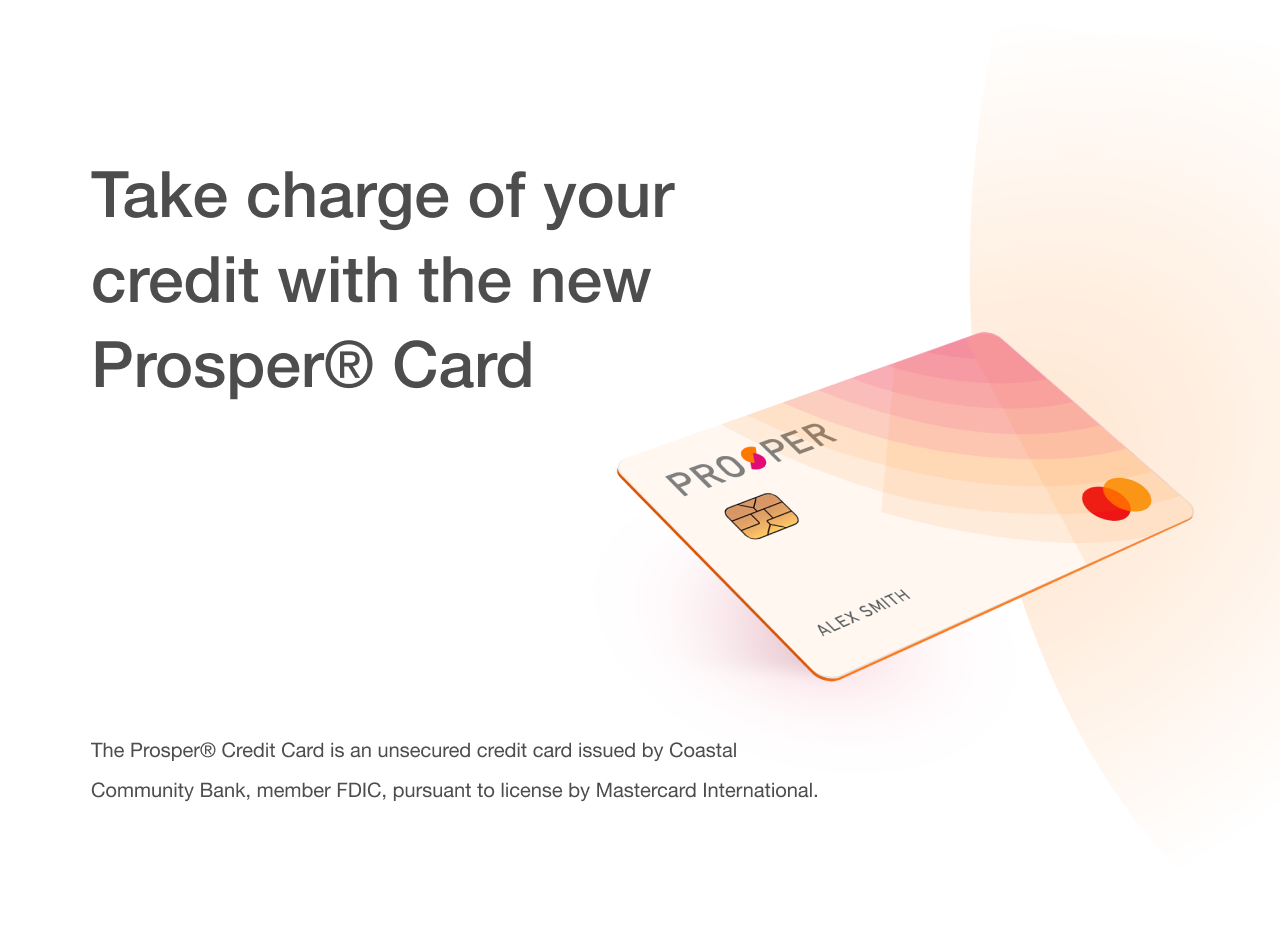

“Consumers working to build their credit profile have historically found it difficult to find an attractive entry point and are often forced to rely on costly alternatives. With the Prosper® Card, people can access the affordable credit they need when they need it, as well as tools and resources to help them stay on track with their personal finances,” said David Kimball, CEO, Prosper Marketplace. “Since launching in 2006, our platform has facilitated $20 billion of affordable credit solutions for more than a million consumers across personal loans and home equity lines of credit, and we are excited to reach even more people with the credit card product.”

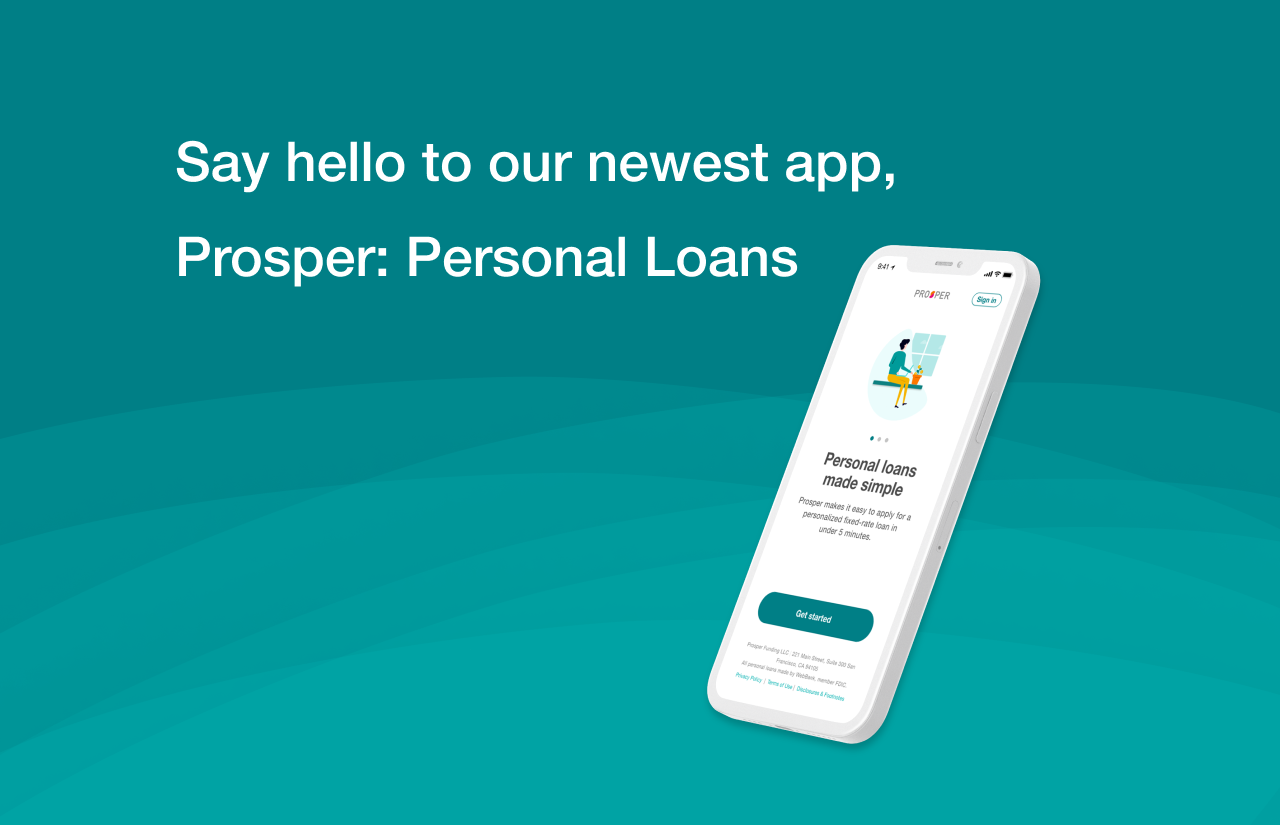

We’re excited to announce the Prosper: Personal Loans App to improve borrower experience! Now you can explore new loan options or manage your existing loan,

Applying for a HELOC has traditionally been a cumbersome process involving a lot of paperwork, long wait times, and trips to the bank. That’s why