“Did you get a good interest rate?”

When applying for a personal loan, that’s the first thing everyone wants to know. The second: what exactly is interest rate vs. APR?

The short answer is this: While finding a low interest rate is undoubtedly important, it doesn’t tell the whole story—especially when it comes to fees, terms, and the total amount you’ll owe over time.

Before applying for a personal loan, you need to understand everything it means for your financial health—and that starts with understanding interest rate vs. APR, or annual percentage rate.

In This Article

Interest Rate vs APR: Interest Rates

What is an Interest Rate?

The interest rate on a personal loan is the amount of money a creditor will earn for lending you money. Think of an interest rate as a fee you pay to access a service—the service of borrowing money.

Expressed as a percentage, lenders apply your interest rate to the total amount of your loan. When you make monthly payments:

- Part of your payment goes to paying back the money you borrowed (your loan principal), while

- The other part goes to your lender as payment for lending you the money (interest, fees).

For example, a loan of $10,000 with an 8.717% APR would ultimately cost you $12,016.66.

If you paid that over 5 years, your $175.28 monthly payment would be:

- $145.48 principal (83%)

- $7.01 interest (4%)

- $21 fees at (12%)

Interest rates are always changing, and they can vary widely depending on the lender and applicant.

How Are Interest Rates Set?

In the U.S., interest rates are set by the Federal Open Market Committee (FOMC). The committee meets eight times a year to assess the economy and determine what interest rate will keep the economy functioning best—aka. what rate will allow people to keep borrowing, lending, and spending money.

Interest rates are then raised or lowered to keep the economy stable and liquid. Liquidity refers to how easily an asset can be turned into cash, and at a price that reflects its true value.

In the U.S., retail banks and lenders also control rates based on the market, their needs, and their customers. While short-term rates are set to create stability and liquidity, long-term interest rates are selected based on demand.

- If fewer people apply for long-term U.S. Treasury notes (10- and 30-year), the rates will be higher.

- If many people want these long-term loans, the rates will be lower.

For example, in early 2022 in the U.S.:

- A short-term (3 month) loan had an interest rate between 0.83 and 0.51%.

- A long-term (10 year) loan had an interest rate of 2.75%.

Applying for a Personal Loan: How is Your Interest Rate Determined?

Personal Loan Lending Factors

Personal loan interest rates can range from 3 to 36 percent. For individuals, these rates vary depending on the details of your loan and your finances.

Lending factors can include:

- Your credit score

- Your current debt load

- Your employment status

- The length of the loan

- The amount you want to borrow

- The reason you’re borrowing money

- The lender you choose

- The type of rate (fixed or variable)

- The type of loan (secured or unsecured)

Fixed Rate vs. Variable Rate

Interest rates on personal loans are either fixed or variable.

Fixed rates remain the same for the length of the loan. With a fixed rate, you know in advance what your monthly payment will be, and the total amount of interest you’ll pay over the life of the loan. Personal loans through Prosper, for example, have fixed interest rates.

Variable rates change over time, which means your interest rate may rise and fall depending on changes in the market. While variable rates may start out lower than similar, fixed-rate loans, you need to be comfortable taking on the risk that your rate could go up at any time.

Secured vs. Unsecured Loan

Personal loans are either secured or unsecured.

A secured loan requires you to put up collateral. That means your lender can take ownership of the asset you put up (property, house, car, stocks, etc.) if you default on the loan.

An unsecured loan allows you to borrow money without putting up collateral. Instead, lenders determine your creditworthiness based on other factors (credit history, income, debt load, etc.).

Most personal loans—including Prosper’s—are unsecured. At Prosper, we offer fixed rates on unsecured loans from $2000 to $40,000, with loan terms of 3 and 5 years.

Applying for a Personal Loan: What are the Benefits?

Personal loans can be used for many purposes, from debt consolidation and home improvements to life events or emergencies. Personal loans are especially helpful when you need access to cash fast.

Key benefits of unsecured personal loans:

- You have flexibility to borrow for most anything you need

- You don’t need collateral

- You can borrow a large amount

- Rates are typically reasonable (and lower than credit cards)

- You know how much you’ll owe each month

- You have time to pay it off and a date when it will be paid-in-full

- You can get your money quickly

Personal loans through Prosper, for example, get funds to borrowers within 5 days on average.

Interest Rate vs APR: Annual Percentage Rate (APR)

Another key factor when applying for a personal loan is the total cost of your loan. Since interest rates don’t include any fees you may be charged during the life of your loan, you need another metric to capture that, which is where the annual percentage rate (APR) comes in.

What is Annual Percentage Rate?

The annual percentage rate is the total cost of borrowing money, including interest and all fees associated with your loan. Like the interest rate, APR is expressed as a percentage that shows you the actual yearly cost of borrowing over the length of your loan.

Because the APR is a bottom-line number, it allows you to compare the amount you’ll owe among different lenders, credit cards, or financial service providers. That’s crucial because, in some cases, a loan with a higher interest rate and low fees could ultimately end up costing you less.

How Do You Calculate APR?

APR is a complicated mathematical formula, so it’s best to use an online calculator to run the calculation.

Gather the following information:

- Your loan amount

- The length of your loan

- Interest rate

- Origination fee

Remember: Lenders are legally required to provide you with your interest rate and your APR as part of any loan agreement, so this information should be easy to find.

Example

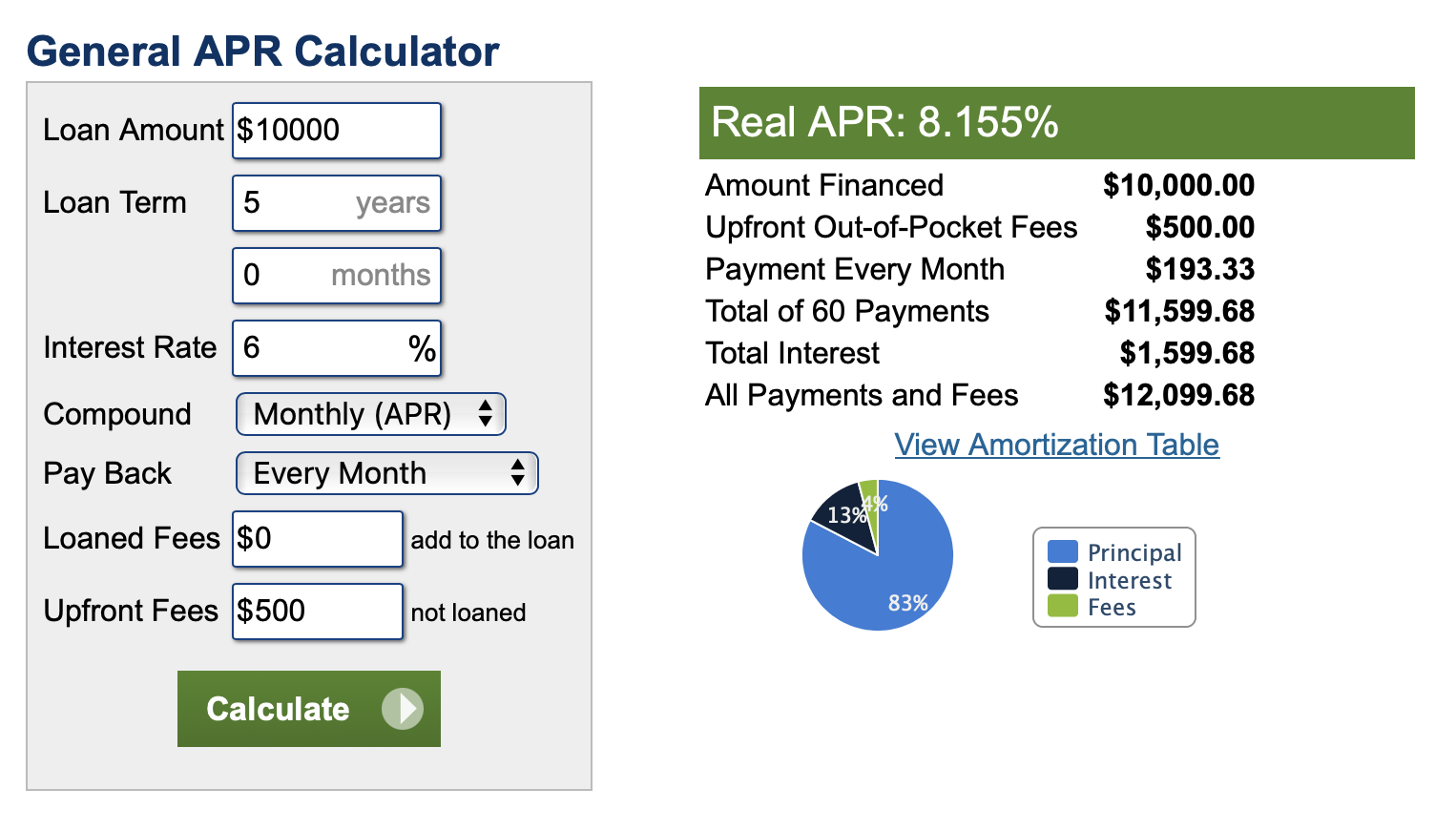

Here’s what the APR looks like on a $10,000 loan.

Source: calculator.net

As you can see, a loan of $10,000 will ultimately cost you $12,099.68 with an 8.155% APR. The lower the APR, the less your loan will cost.

What is an Origination Fee?

The most common fee charged by lenders is an origination fee, which reimburses lenders for performing due diligence (pulling your credit report, verifying supporting documents, etc.) Some lenders charge a set dollar amount, while others structure the fee as a percentage of your loan amount. Online lending platforms like Prosper, for example, charge origination fees ranging from 1%-7.99% depending upon your credit rating.

Example

Let’s say you borrow $10,000, and your lender charges an origination fee of $500. Depending on your loan and lender, the origination fee:

- May be taken out of your loan (you borrow $10,000 and receive $9,500), or

- May be charged in addition to your loan (you borrow $10,500 and receive $10,000 in funds).

Either way, the origination fee affects your loan’s bottom line. While an offer to waive the origination fee is enticing, be sure to look at the interest rate and other fees to see the total cost. Chances are, waiving the origination fee just means the company is making the money back somewhere else in a less obvious fashion.

What Does It Mean When Lenders Advertise “No Fees”?

To that end, remember that transparency is important when making major financial decisions. Many lenders like to advertise that they charge “no fees” for their loans, which sounds like a pretty sweet deal. And while it’s true that you may never see a line item on your statement for origination or processing fees, you are still being charged for that labor.

Whether you’re paying the origination fee over time (ex. in higher monthly payments) or whether it comes out of your loan total at closing, that fee is coming out of your pocket one way or another—the only difference is how and when it’s happening.

Ready to Start Applying for a Personal Loan?

Now that you understand interest rate vs APR, you’re ready to explore your options. To find out whether you qualify, check out our easy-to-use personal loan calculator.

All personal loans made by WebBank.