Continued Resilience and Strong Credit Performance

Prosper’s Q1 2021 Quarterly Update provides our investor community the latest information on the performance of loans on the Prosper platform as well as our view of the macro environment. Overall, we have continued to see improvement in credit performance on the Prosper platform driven primarily by our disciplined underwriting approach over the past several years. We believe this is also a testament to the strength and resilience of Prosper’s platform, which leverages over 10 years of proprietary data along with sophisticated AI-driven models using traditional and alternative data sources to evaluate credit and fraud risks.

Current macro-economic environment

Due to unprecedented government stimulus over the last year, the overall macro environment is showing ongoing signs of improvement. Additionally, due to reduced consumer spending, consumer finances for middle and high-income borrowers appear to be in better shape today vs pre-pandemic, as demonstrated by the following data:

- The unemployment rate in February 2021 was at 6.2%. While current unemployment rate is still high relative to February 2020 unemployment rate of 3.5%, it has improved materially since the peak unemployment rate of 14.8% in April 2020[1].

- Employment rates among workers in the top wage quartile (those making greater than $60K annually) is better than pre-pandemic levels[2].

- Revolving balances on credit cards and other revolving plans in February 2020 are down by 13% ($114B) year-over-year due to reduced consumer spending[3].

- Personal savings rate, defined as personal saving as a percentage of disposable personal income (DPI), is at 20.5% in January 2021 vs. 7.6% in January 2020, amounting to over $2.6 Trillion in higher savings year-over-year, mostly concentrated in middle- and high-income households[4].

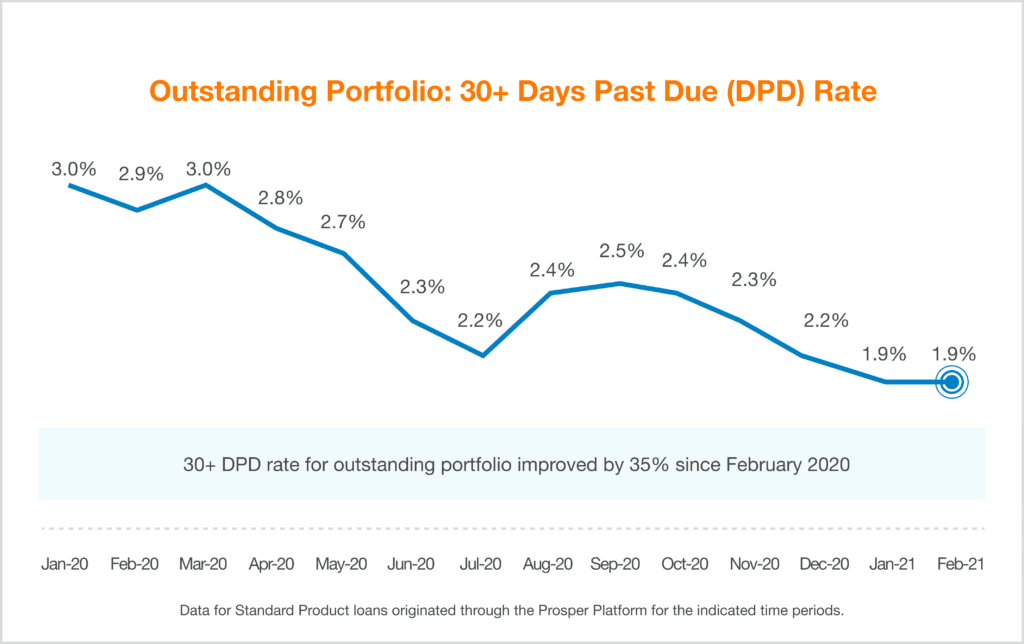

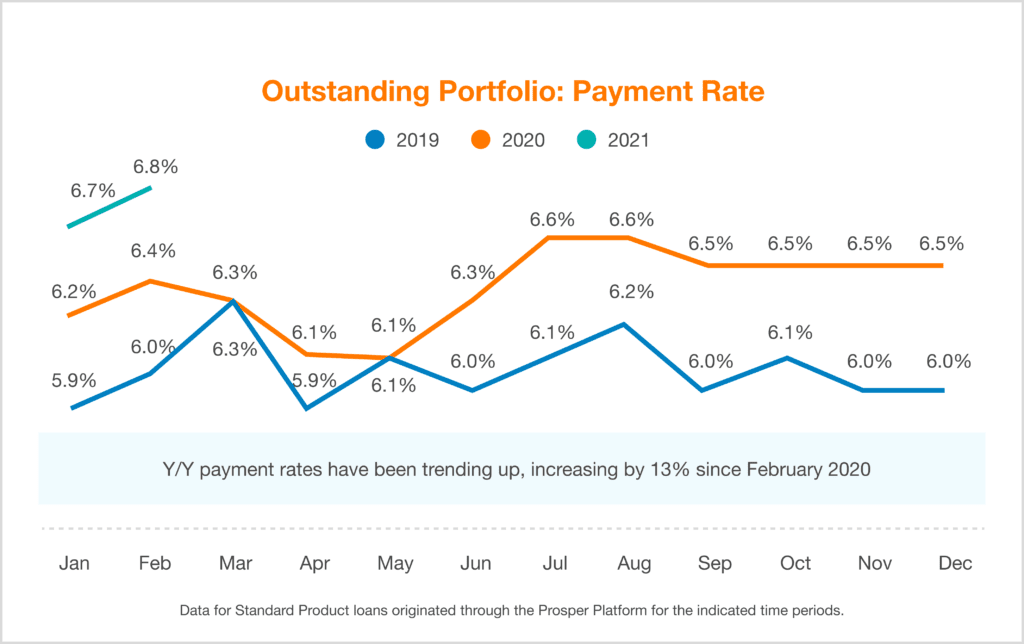

Outstanding Portfolio Performance

Overall, performance of our outstanding portfolio is trending better than pre-pandemic levels.

- 30+ Days Past Due (DPD) rate for our outstanding portfolio is 35% favorable to February 2020 levels and overall payment rate on the portfolio is 13% higher compared to the prior year.

- As of February 2021, 3.8% of outstanding receivables are enrolled in a Prosper COVID-19 relief program. Almost all of these borrowers are enrolled in a payment reduction program.

- 80% of borrowers graduating from their payment reduction period are staying current by either making new higher payments or enrolling in a second stage of the payment reduction program, which provides an additional six-month payment reduction period.

- Performance of borrowers who did not enroll in any of our COVID-19 hardship relief programs continues to trend favorably; 30+ DPD rate for these borrowers is 44% lower than pre-pandemic levels.

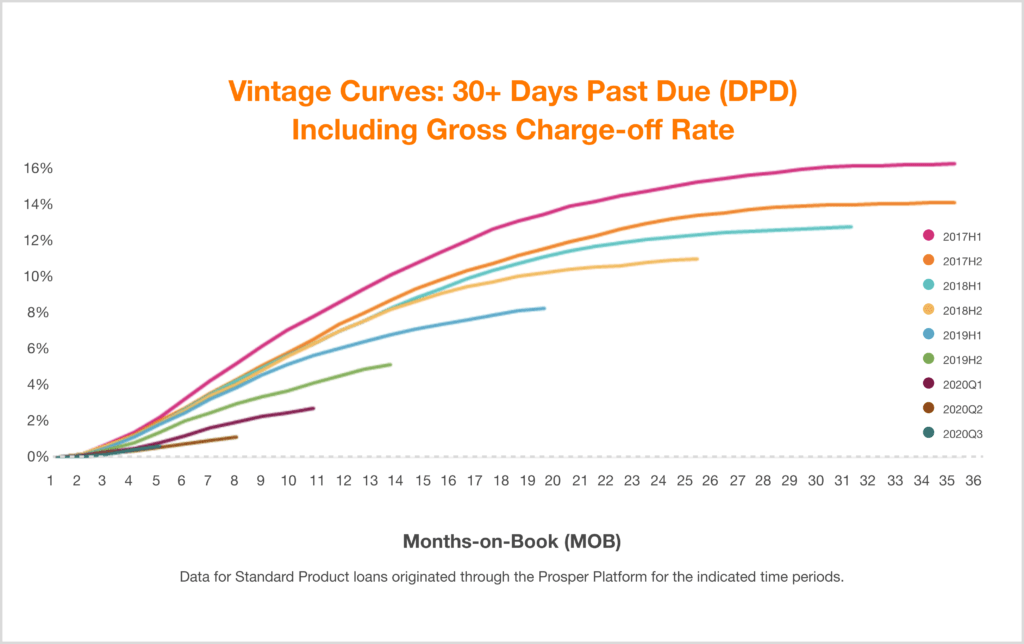

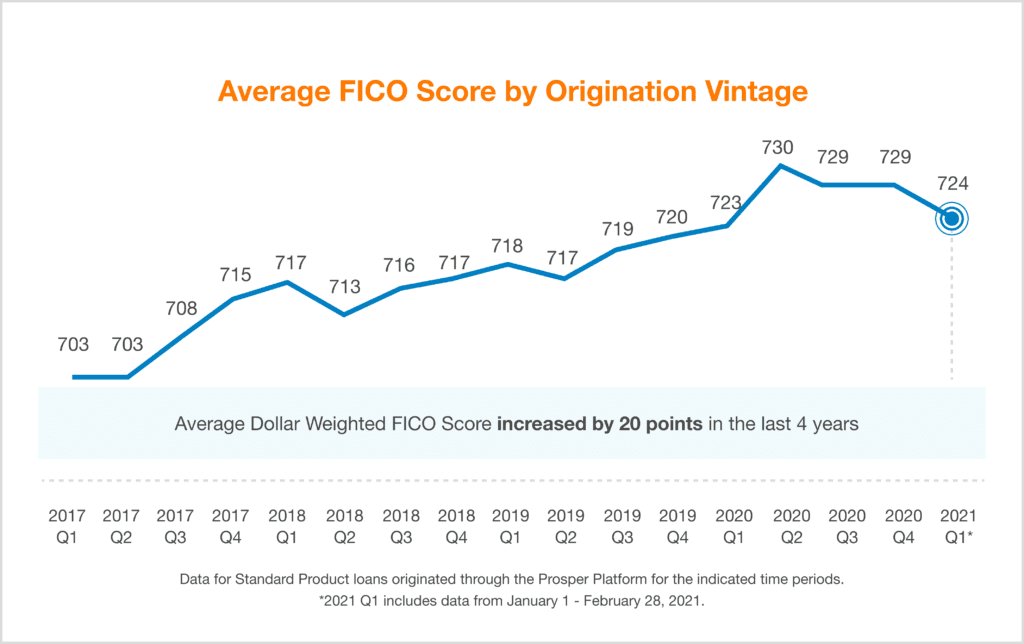

New Originations Credit Quality and Early Performance

- Early delinquency rate for vintages underwritten just before the pandemic (2019H2, 2020Q1) as well as vintages underwritten during the pandemic (2020Q2, 2020Q3) is trending favorably.

- Credit quality of new originations continues to be strong year-over-year. Repeat borrowers, who have historically demonstrated significantly better credit performance than new borrowers, made up 53% of originations in February 2021 vs. 45% in February 2020.

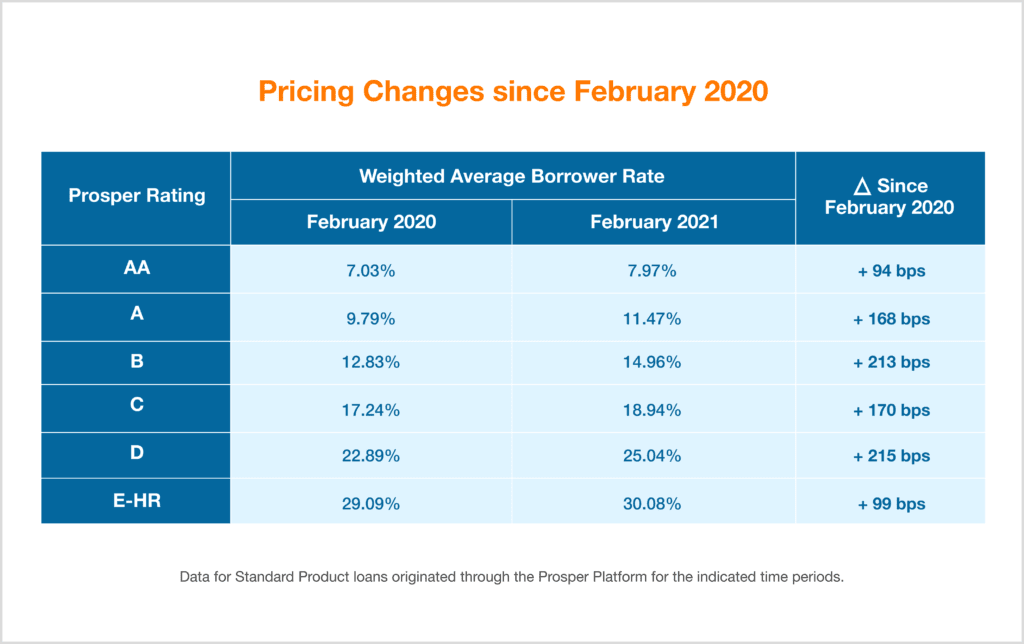

- Compared to pre-pandemic levels, borrower rates on the platform remain higher to help provide enough cushion to platform investors against volatility in the macro environment.

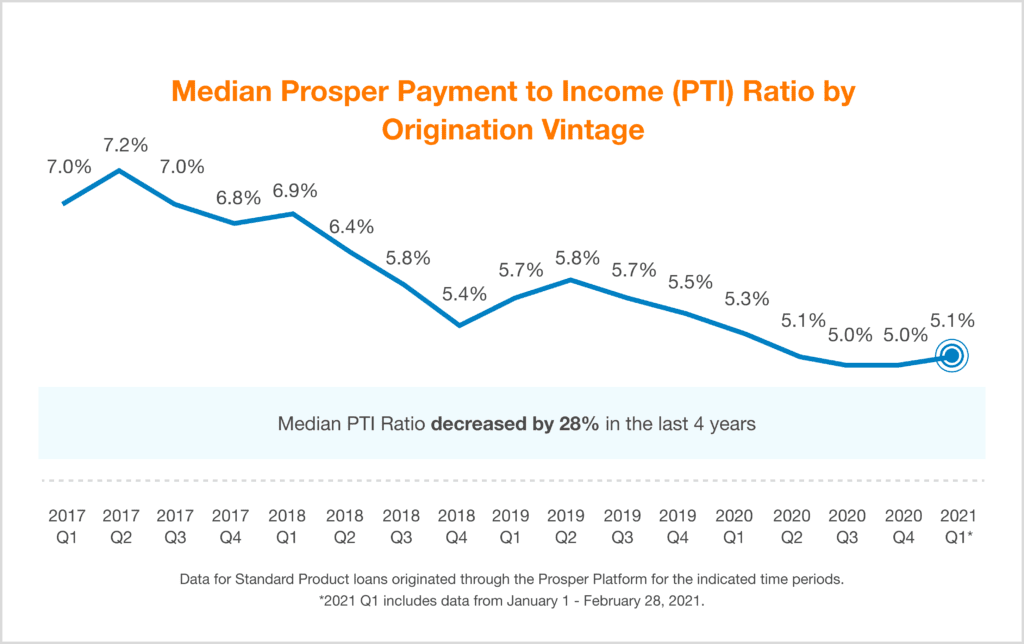

- Median monthly loan payment to income ratio (PTI) was 5.08% in February 2021 vs. 5.31% in February 2020.

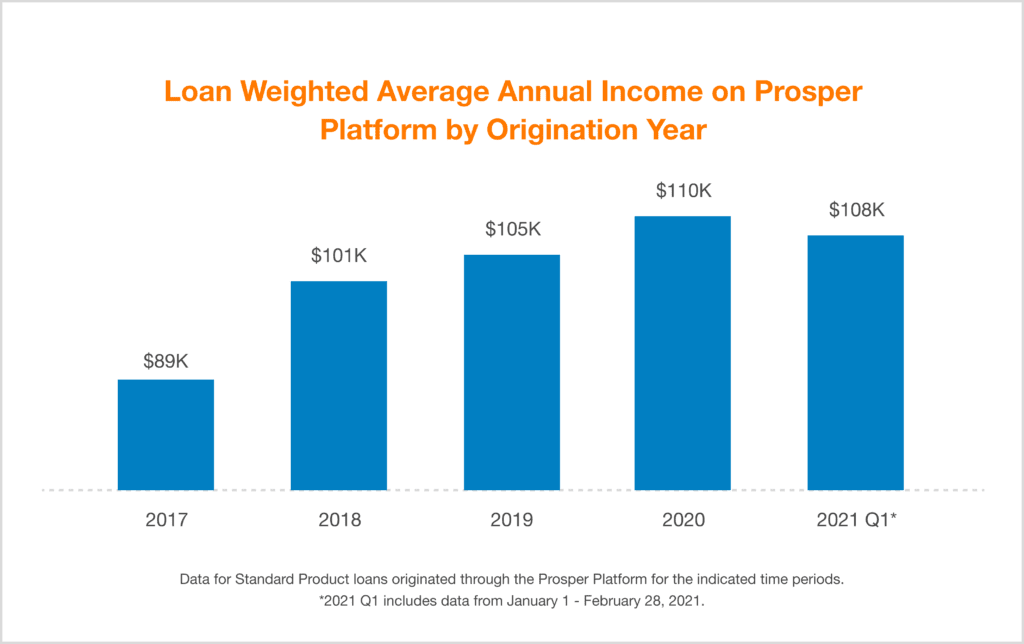

We believe our consistent focus over the last several years on higher credit quality and higher income borrowers has contributed towards the resilient credit performance we’re seeing on the Prosper platform and helped us deliver solid risk-adjusted returns for our investors. We continue to remain disciplined in our approach in a dynamic credit environment.

[1] https://fred.stlouisfed.org/series/UNRATE

[2] https://tracktherecovery.org

[3] https://fred.stlouisfed.org/series/CCLACBW027NBOG

[4] https://fred.stlouisfed.org/series/PSAVERT

All data on this blog post is presented for informational use only. This data is impersonal and is not directed to the specific investment objectives, financial situation or investment needs of any particular person, and should not be considered investment advice. This information is not intended to be, nor should you interpret it to be, a prediction of how any particular portfolio will actually perform. You should always carefully consider investments in any security and you should be comfortable with your understanding of the investment prior to investing. Actual results may vary.

This blog post includes forward-looking statements. Forward-looking statements may include financial and other projections; statements about the impact of our credit and underwriting initiatives and our ability to successfully navigate the current macro-economic environment; statements regarding investor returns, loan performance, and the impact of the current pandemic; as well as the assumptions underlying any of the foregoing. Forward-looking statements inherently involve many risks and uncertainties that could cause actual results to differ materially from the plans, intentions and expectations in these statements, and there can be no assurance that the expectation or plan will result or be achieved or accomplished. All forward-looking statements speak only as of the date of this blog post and are expressly qualified in their entirety by the foregoing cautionary statements. We undertake no obligation to update or revise forward-looking statements that may be made in this blog post to reflect events or circumstances that arise after the date made or to reflect the occurrence of unanticipated events.

Prosper’s borrower payment dependent notes (“Notes”) are offered pursuant to a Prospectus filed with the SEC. Notes are not guaranteed or FDIC insured, and investors may lose some or all of the principal invested. Investors should carefully consider the risks, uncertainties, and other information described in the Prospectus before investing.