Blog · 5min read

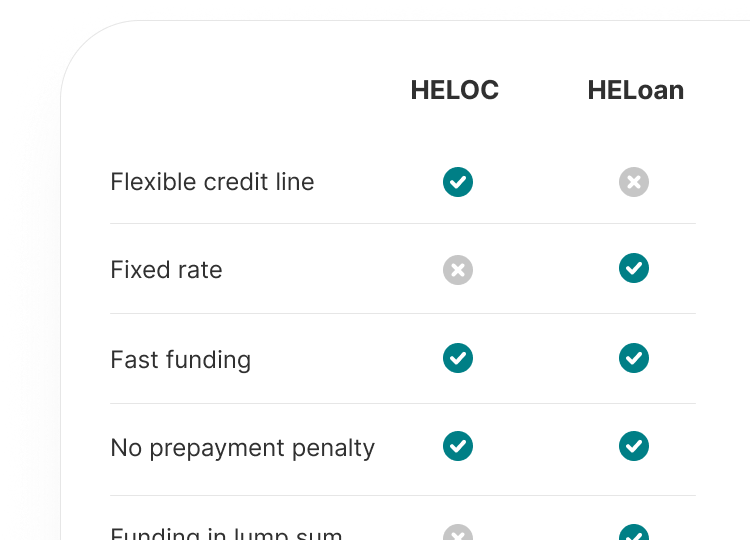

Home equity loans vs. lines of credit

These are two popular financing options that allow you to draw on the equity you’ve built in your...

Read more

Use this calculator to help estimate your personalized interest rate, payment, and loan amount with a home equity loan (HELoan) through Prosper.

Est. variable rate1,5

0%

Est. credit line4

$0

Est. monthly payment1,5

$0

Est. fixed rate

0%

Est. loan amount7

$0

Est. monthly payment6

$0

Est. variable rate1,5

0%

Est. credit line4

$0

Est. monthly payment1,5

Est. mo. payment1,5

$0

Est. fixed rate

0%

Est. loan amount7

$0

Est. monthly payment6

Est. mo. payment6

$0

Enjoy our no-stress, speedy digital process

Enjoy our no-stress, digital process

This calculator is a self-help tool for your independent use and is intended for illustration purposes only. Results aren’t guaranteed, and may not be relevant to your specific circumstance.

We've got your back, every step of the way.

Chat with a dedicated Prosper team member, not a robot.

Answers to home equity questions, from your application to payments.

Home equity is just the beginning. Prosper has smart, simple tools for borrowing, saving, and earning with products like personal loans, a credit card, and investing.

About Prosper